The forecast is based

on the historical data, past information, experience and knowledge of recent

events that are likely to affect the future oil and gas markets. Despite a

large amount of information and knowledge, forecasting prices is always

uncertain and unpredictable. Benjamin Disraeli: ‘What we anticipate

seldom occurs, what we least expected generally happens’.

In March 2005, Goldman Sachs said oil could top $100 a barrel, dubbing the

phenomenon a "super spike." But in June 2005, an economist from Morgan Stanley predicted oil prices

could collapse.

The New York Times December 4, 2005. “Some oil executives worry prices

may fall” Cheap oil may once again be just around the corner. Even as

consumers worry about high gasoline prices and rising heating bills, oil

executives in London, Texas

and Saudi Arabia

seem to be concerned about the prospect of falling oil prices.

In a recent speech in Singapore,

John Browne, the chief executive of BP, spoke of a possible sharp drop in

prices and called current levels "unsustainably high."

John Hofmeister, head of Shell Oil in the United States, said during an

interview, "This high price cycle is artificially inflated."

The Observer January 1,

2006 “Bosses predict year of pain”. In the survey of

more than 100 FTSE top executives, MORI found that 66% expect the economy to

worsen in 2006, while 4% believes it will improve. Analysts expecting rampant US growth to

shutter in 2006, little sign of recovery in Euro Zone, and consumer spending at

home still under pressure from rising taxes, businesses have plenty of reasons

to be nervous about the year ahead. The economic climate worried 17% of

executives, with the chairman of a leading mining and natural resources company

citing “uncertainty in the pattern of economic development in China”,

as a concern. Manufacturing sector suffered in 2005 as demand from Euro Zone

remained weak, and high energy prices took their toll.

Danger time for America.

“The economy that Alan Greenspan is about to hand over is in much less

healthy state than is popularly assumed” (The Economist January 12, 2006).

Saudi Arabia's oil minister, Ali al-Naimi, said recently at a news

conference in Riyadh, "As producers, we don't want to build capacity

without demand" – referring to 1998 financial crisis that resulted

in glut in production capacity, sluggish demand that led to oil-price collapse

with futures contracts falling to about $10/barrel.

Despite these headline grabbing reports, most economists and energy

analysts are of the view that the price of oil will probably float between low $40

a barrel and the high $60s for the foreseeable future.

So who’s right? Well, maybe no

one!

Can we live without forecasting?

The forecast we make today is based on best available information, past

experience and the most recent events that influence the oil, gas sector and the

global economy. Nevertheless projecting oil price is always uncertain and

unpredictable. The reasons being that oil price forecast is a complex issue and

dependent on host of factors, some of which are beyond human control. If the

future is uncertain and frequently our forecast turns out to be wrong then why

one makes forecast? Can we live without it? The answer is ‘Yes’ and ‘No’. Despite

the elements of uncertainties, international agencies, multinational oil

companies and consultants do have to forecast. To analyze the potential level

of risk in decision making and to reduce the element of uncertainty in

forecasting, analysts also consider options such as “scenario analysis” which

is a function of the lessons learned, most recent events, and future

perception.

Have we learned from past episodes?

The lessons learned from the past also play an important contribution in

formation of probability distribution and future expectations. George Boole “Probability

is expectation founded upon partial knowledge. A perfect acquaintance with all

the circumstances affecting the occurrence of an event would change expectation

into certainty, and leave nether room nor demand for a theory of probabilities”.

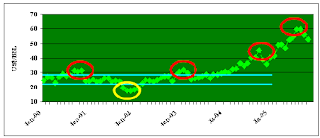

Figure-1 highlights the historical trends of oil prices. At a glance by

visual inspection of the historical trends it is noted that generally oil price

shocks of 1970’s, 1986, 1990 and 1997 were short lived and world oil prices

quickly adjusted or converge towards the historical average prices with slight

variations. For example during 1986 to 2003 oil prices were generally stable

and on an average remain in the twenties. In view of the stability in that

period, predicting oil prices was not as complicated. One important conclusion that can be inferred

from visual inspection of historical trends – generally oil price shocks (both

negative and positive) are short-lived – normally stretching over one-two

years, except for 1973, and eventually quickly converge towards the historical

average due to market fundamentals.

Figure 1: Historical trends of world oil price – 1970/2005

Factors

affecting short-term oil price movements

Most recently oil prices increase strongly in 2004. For example, WTI

increased from $31.16/BBL in 2003 to $41.44/BBL in 2004 and an even more robust

trend was witnessed during 2005 when average annual price increased to $56.47/BBL

(Figure-2). Many factors were responsible for the exceptionally high oil prices

during 2004/2005. The low level of US stocks, high demand, strikes in

Venezuela, civil unrest in Nigeria, refining constraints, hurricanes, insufficient

production capacity due to inadequate investment in the past and fear of supply

disruption due to increasing insurgency in Iraq have certainly contributed to

this unusual elevation in oil prices (Figure-3).

For example, in 2004, China’s oil demand increased by about one million barrels

daily (MMBD) due to surge in car sales owing to easy credit and hot summer that

led to increases usage of diesel generators owing to shortage/rationing/load

shading of electricity. The price of WTI after the Hurricane Katrina increased

to over $ 70/bbl in late August 2005, an all time record in nominal terms and the

highest price since 1981 in real terms (shutting down production platforms,

refineries, pipelines, oil ports in the region affecting security of supply at

least in the short term). Since the introduction of OPEC price band of

$22-28/bbl in February 2000 to January 2005, 47 percent of the times OPEC

managed to stabilize oil prices within its price band, while 8 percent of the

times it was under $22/bbl and 44 percent over $28/bbl. In fact since October

2003 the OPEC basket remains exceptionally higher than the upper band of $28/bbl

forcing OPEC in their 134th meeting to temporarily suspend the price band.

Figure 2: OPEC basket price movement – monthly (nominal terms).

Figure 3: Some factors influencing short-term oil price movements.

How most recent events alter

expectations?

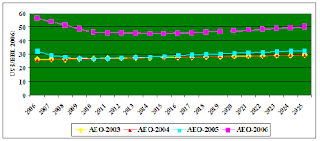

We also make an attempt to compare forecast of oil prices published by international

agencies in 2003, 2004, 2005, and 2006 and analyze how the expectations have

changed as more information becomes available. Figure-4 draws out the

comparison of Energy Information Administration (EIA’s) Annual Energy Outlook

(AEO’s) for the years 2003, 2004, 2005 and 2006 (All previous years oil price

forecast have been converted into 2006 dollars for ease of reference). Up until

AEO 2005, EIA’s long-term price forecast more or less remains below $30/BBL.

However this perception changes in AEO-2006 due to persistently higher oil prices

during 2004/2005. EIA’s forecast is significantly stronger as compared to their

previous forecasts. The current oil prices expected to decline marginally to

56.42 in 2006. The prices in the succeeding years expected to continue observe a

gradual declining trend – reaching 44.96/BBL in 2015. Thereafter, oil prices

gradually increases and by 2025 reaches $50/BBL. That is throughout the

forecasting period EIA predicated that world oil prices are likely to hover

around mid-to-upper forties –much stronger than their AEO-2005. It should be

noted that there has been a significant shift in EIA’s thinking about the

future long-term oil price path and all other underlying parameters as compared

to their previous year’s forecasts. EIA is now of the view that oil market is

likely to remain tight during 2006/2025. A strong oil demand is expected in the

USA, China and emerging economies of Asia while combined oil production capacity of OPEC and

non-OPEC is not likely to come forth as previously anticipated – therefore

EIA’s view that oil prices likely to remain between mid-forties to fifties.

Figure 4: Energy Information

Administration World Oil Price Forecast – various Annual Energy Outlook (AEO)

in 2006 $

The Purvin & Gertiz (P&G) predicting that world oil prices in 2006

is likely to remain on the higher side at around $61.63/BBL and then decline

sharply in the next 2-3 years before making a gradual decline reaching at

$34.6/BBL by 2012 (Figure-5). The reason for higher oil price forecast this

year is primarily due to the strong cost pressure on the industry. Their model

predicated that oil prices then likely to gain strength and move gradually

reaching at around $39.72/BBL by 2025. P&G forecast revels that world oil

prices are likely to be remaining within the mid-thirties dollars in real 2006

dollars

.

Figure 5: Purvin &

Gertiz long-term price

forecast

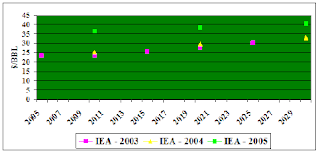

Likewise

International Energy Agency (IEA) also revised its long-term oil price forecast

in 2005 due to persistent higher oil prices in most recent years. IEA oil price

path also shows a declining trend in the years to come reaching at the bottom

at around 2015 and then rises. Throughout the forecast period it appears that

IEA’s expectation are that oil prices most likely expected to remain within

$35-40/BBL (Figure-6). In reference scenario, the price is assumed to ease to

around $35/BBL in 2010 as new crude oil production and refining capacity comes

on stream. It is then assumed to rise slowly, in more or less liner way, to close

to $37 in 2020 and $39/BBL by 2030. The higher oil-price path assumed here than

in World energy Outlook-2004 (WEO) reflects, in part, a recent shift in

producing countries’ price objectives. The assumed slowly rising trend in real

prices after 2010 reflects as expected increase in marginal production costs

outside OPEC, an increase in market share of a small number of major producing

countries and lower spare production capacity. Therefore most of the

incremental demand is expected to be met by OPEC members, mainly in the Middle East. This will increase reliance on OPEC oil and

their ability to influence oil prices. In the reference case it is assumed that

OPEC will not increase oil prices too high and too quickly to avoid reduction

in global oil demand as well as accelerating the development of alternative to

hydrocarbons.

Figure 6: International Energy Agency (IEA)

long-term oil price

forecast

Comparison of latest oil price forecast

Despite difference in magnitude all the three forecasts shows a similar

pattern of declining trend reaching to lowest level to around 2015 followed by

a period of strengthening (Figure-7). The trends also show how the expectations

are changed due to changes in the most recent events particularly that of

status of most recent oil prices. EIA’s perception about the future is tight

market and therefore sees stronger oil prices as compared to others.

Figure 7: Comparison of long-term oil price forecast (2006$)

Why

one see downward oil price movement?

David

O’ Reilly, the chief executive of Chevron, said “High prices tend to

attract higher production and higher supplies. The question then is what will

happen to the demand side? The fact is, we rarely know what is going to happen”.

History

has taught us that continual higher oil prices encourage exploration and

conservation. The first and most important determinant of the level of

exploration activity by international oil companies (IOCs) is the current and

most recent past oil prices. The initial response of the industry to increase

oil prices may not immediately lead to an upsurge in exploration activity, but

possible a reappraisal of discoveries made in mature regions deemed uneconomic

under previous price scenarios. Therefore, exploration activities in new

acreage especially high-risk-high-cost basin are expected to increase after a

year or two in response to current higher oil prices especially if IOC’s

strongly view that current pattern of oil price continue in the future. Oil

companies increase their exploration activities on anticipation in growth in

demand and favorable oil price regimes in the future. Based on these prospects,

these companies are willing to invest in high cost unexplored basins in search

for sizeable oil fields. Increasing exploration activities in new frontier area

will eventually increase oil reserves and production.

In

addition current high oil prices are likely to induce investments in energy

efficient systems; backstop fuel supplies from unconventional crude oil from

tar/tight sands, oil shale, gas to liquid (GTL), coal to liquid (CTL),

clean coal technology and other renewable sources of energy – thus reducing the

pressure on oil demand in the long run. Persistent higher oil prices on the one

hand, increase the supply of crude oil (increase in exploration), increase in

unconventional and renewable sources of energies, and on the other hand, it

will likely to adversely affect the global economy – slowing down oil demand.

Therefore, eventually market forces may push the oil prices downward. Although current higher oil prices have shown

that the global economy has the capacity to withstand un-expected upward surge

in oil prices of this magnitude. However it remains to be seen if this

resilience in the economies can be sustained over an extended period. An

attempt is made in this short paper to assess some of the factors that are

likely to influence future expectations/price forecast. However to comprehend

the subject it requires further depth analysis of each of the underlying

parameters discussed in this paper

Conclusions

Although future is uncertain and highly unpredictable, we do attempt to

forecast oil prices---short and long-term. This analysis could benefit business

plan preparation, investment decision in exploration and development,

feasibility studies, preparing budget, etc. The objective is try to form

expectation based on history, most recent events and how one expect the basic

parameters likely to change in different conditions: economic, geo-political,

environmental and technological breakthroughs. Even though with all the

endeavors, experience and wisdom what we forecast seldom takes place, instead

what least expected happens. Our thrust of learning about the future does not

diminish and we continue to form expectations and carry on with forecasting.

Subsequent events can further review the accuracy of these results. However the concept of scenario analysis

provides an added dimension – defining the band within which oil prices can move

during a particular time period to facilitate the decisions making process.

References:

Jad Mouawad, The New York Times. December 4, 2005. “Some Executives worry prices may fall?”

Energy Information Administration (EIA) various Annual Energy Outlook

International Energy Agency – various reports on World Energy Outlook

Remarks by Governor Ben S. Bernanke, October 21, 2004. At the Distinguished Lecture

Series, Darton College,

Albany, Georgia.

Paul R. La Monica, CNN/Money series writer. July 6, 2005. “Debate raging over oil”.

Ghouri Salman. September 2005. “A

Dilemma of Oil Prices - Short Memories”. PetroMin.

Robert Worcester and Heather Stewart. January 1, 2006. “Bosses predict year of pain”,

The Observer.

Purvin & Gertiz long-term crude oil price forecast, The Economist,

January 12, 2006.

Note: This

paper was published in PetroMin (March 2006 - Website: www.safan.com – The purpose of sharing this paper

is to review our recent past memories and our perception about future

technological development without compromising the basic market fundamentals.